Deposit Procedures

Table of Contents

GENERAL CONCEPTS

Overview of Collection and Deposit Process

Responsibility for Internal Control

DEFINITIONS

Collection Point

Collection Custodian

Deposit Processing Point

Deposit Custodian

Depository Bank Accounts

RECEIPT, DEPOSIT AND RECONCILIATION OF FUNDS COLLECTED

Guidelines for Cashiers and Collection Custodians

- Cash Collections

- Check Collections

- Credit and Debit Card Collections

- Verification and Delivery of Funds Collected to Deposit Custodian

- Collection Procedures

Guidelines for Deposit Custodian

- Verification and Receipt of Funds Collected from Collections Custodian

- Daily Reconciliation to Bank Activity Report

- Deposits of Funds Collected

- Cash Receipt Preparation

- Collection Procedures

WRITTEN COLLECTION AND DEPOSIT PROCESSING PROCEDURES

General Requirements

Informational Requirements

- Basic Information

- Supporting Documentation for Collections

- Daily Operations, Reconciliation, and Balancing

- Segregation of Duties and Internal Controls

- Safeguarding of Funds

- Training of Personnel

GENERAL CONCEPTS

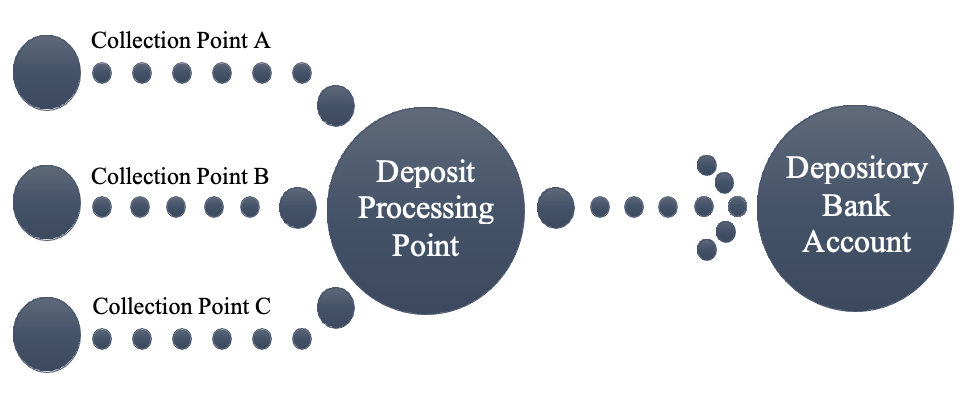

Overview of Collection and Deposit Process

Revenue to be deposited into TTUHSC bank accounts is received by multiple departments and at various locations within TTUHSC. The diagram below presents a general flow of revenue deposits into TTUHSC depository bank accounts.

Revenue deposits are recorded in TTUHSC's Banner Finance System utilizing the Cash Receipts system per HSC OP 50.26 Use of Online Cash Receipts System . Training regarding the use of the Cash Receipts system is available under the Help menu within that system in the Cash Receipts Help document. Gifts for the benefit of TTUHSC that are processed by Texas Tech Foundation Inc. do not utilize the Cash Receipts system.

Responsibility for Internal Control:

Establishing and maintaining internal cash controls for each collection and deposit processing point is critical to prevent the mishandling of funds and to safeguard against loss. Strong internal controls also protect employees from inappropriate allegations of mishandling cash and other forms of payment by defining assigned responsibilities in the collection process.The appropriate Vice President, Dean, or Regional Dean with responsibility over operations that include collection and deposit processing points bears the responsibility for general oversight and guidance to foster an environment that ensures that internal controls are established and followed. These individuals should regularly review written Collection Procedures to ensure that established controls are adequate.

Fund managers are ultimately responsible for the financial and operational management of their funds, including establishing internal controls at the department level and verifying that deposits are properly posted to their funds per HSC OP 50.03 Financial and Fund Manager Responsibilities. Thus, fund managers should be aware of collection procedures for their respective deposits, including review of the written Collection Procedures.

Collection and Deposit Custodians are responsible for periodic reviews of the collection and deposit process to ensure that segregation of duties and adequate controls are in place and are being properly followed by the respective custodian and other cash handlers.

Vice Presidents, Deans, Regional Deans, fund managers, deposit custodians, and collection custodians should continually consider possible cash vulnerabilities and resolve concerns immediately. Accounting Services, Business Affairs, or Audit Services may be contacted at any time for assistance.

All collections of cash and other forms of payment must be recorded in the Banner Financial System and deposited into TTUHSC depository bank accounts. Anyone with knowledge of off-the-book transactions should immediately notify the Vice President and Chief Financial Officer or the Director of Accounting Services.

No person at the institution has the right to circumvent state law. If it is discovered that state law is being violated, disciplinary action will be taken in accordance with Regents' Rules, Section 07.03, Fraud Policy. Every employee has the responsibility for contacting Audit Services, Accounting Services, and the Texas Tech Police Department to report possible fraudulent acts if there is a reasonable basis.

DEFINITIONS

Collection Point: A location involved in the regular collection of cash, checks, credit cards, or other forms of payment is a Collection Point. A Collection Custodian should be appointed at each Collection Point.

Collection Custodian: The Collection Custodian is responsible for establishing and overseeing payment handling procedures at the Collection Point. Responsibilities of the Collection Custodian include:

- Following the procedures outlined in this Deposits Procedures Manual.

- Establishing written Collection Procedures.

- Overseeing cash fund(s) established at the collection point per TTUHSC OP 50.21 Cash Funds.

- Completing and passing the Cash Fund Training provided by Accounting Services.

- Ensuring that supporting staff are trained to follow established procedures. This training could include, but is not limited to, cash fund training provided by Accounting Services and control environment, cash controls, and fraud awareness training developed by Audit Services.

- Daily balancing of cash and other forms of payment to supporting documentation.

- Submitting timely deposit information and supporting documentation to the Deposit Custodian.

Deposit Processing Point: A location that receives funds from collection points, prepares deposits and related cash receipts, and is responsible for the actual deposit of funds into TTUHSC Depository Bank Accounts is a Deposit Processing Point. A Deposit Custodian should be appointed at each Deposit Processing Point.

Deposit Custodian: The Deposit Custodian is responsible for establishing and overseeing deposit procedures at the deposit processing point. The Deposit Custodian should be someone other than a Collection Custodian and should not be involved in collecting cash or other forms of payment, opening mail, or other payment collection duties. General responsibilities of the Deposit Custodian include:

- Following the procedures outlined in this Deposits Procedures training.

- Establishing written deposit processing procedures.

- Ensuring that supporting staff are trained to follow established procedures. This training could include, but is not limited to, cash fund training provided by Accounting Services and control environment, cash controls, and fraud awareness training developed by Audit Services.

- Verifying deposit information and supporting documentation received from the Collection Custodian.

- Preparing deposits and related cash receipts to record deposits in the Banner Finance system.

- Ensuring that deposits are made to TTUHSC Depository Bank Accounts promptly.

- Establishing procedures to reconcile daily deposits to the related Bank Activity Report.

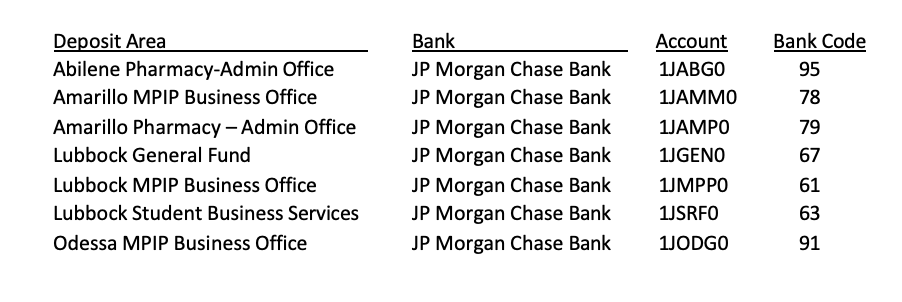

Depository Bank Accounts: TTUHSC depository bank accounts facilitate deposits for regional campuses or other specialized areas within the institution. Establishment of all TTUHSC bank accounts must be approved by Accounting Services. Further, the use of unauthorized bank accounts is strictly prohibited.

Below is general information on the seven depository accounts currently in use for TTUHSC:

RECEIPT, DEPOSIT AND RECONCILIATION OF FUNDS COLLECTED

Guidelines for Cashiers and Collection Custodians:

- Cash Collections

- Cash funds should be managed in accordance with the related Cash Fund Control Plan and in accordance with HSC OP: 50.21, Cash Funds.

- Only one cashier should be allowed access to a cash register or cash drawer during a single shift. If funds are passed from one cashier or custodian to another, transfer of accountability and cash count verification should be documented and signed by both the transferring and receiving cashier or custodian.

- Collection of cash in person should be recorded on a point-of-sale register or terminal when available, and a register receipt provided to the paying customer. If a point-of-sale register or terminal is not available, then pre-numbered receipts should be utilized, and a copy of the receipt should be provided to the paying customer. Voided receipts should be approved and initialed by the appropriate Collection Custodian.

- Cash received via mail should be recorded on a mail log, which will serve as supporting documentation for receipt of payment.

- Cash collected should be balanced daily by comparing total cash on hand to cash register totals, pre-numbered receipt totals, and mail log totals as applicable.

- Check Collections

- Collection of checks in person should be recorded on a point of sale register or terminal when available, and a register receipt provided to the paying customer. If a point-of-sale register or terminal is not available, then pre-numbered receipts should be utilized, and a copy of the receipt should be provided to the paying customer. Voided receipts should be approved and initialed by the appropriate Collection Custodian.

- Checks received via mail should be recorded on a mail log, which will serve as supporting documentation for receipt of payment.

- All checks received should be endorsed immediately with a restrictive TTUHSC endorsement stamp per HSC OP 50.10 Endorsement Stamps and Endorsement of Checks.

- Checks should contain the following information before the check is accepted for payment:

- Payable to Texas Tech University Health Sciences Center (TTUHSC) or to the department name followed by TTUHSC.

- Signature of the payer

- Current date

- Amount that agrees with the payment amount due. Checks written for more than the amount due should not be accepted.

- Notation indicating the service or goods for which payment is made

- Driver's license information of the payer, verified by review of the driver's license

- Imprint of magnetic ink characters for account identification at the bottom of the check

- Payer's preprinted name and address of the payer. Acceptance of temporary checks with handwritten payer information is discouraged.

- Any check drawn on a foreign country bank must be sent to the Student Business Services office. Checks drawn on foreign banks will not be considered as payment until the funds are actually collected.

- Postdated, third-party, or altered checks should not be accepted.

- Checks collected should be balanced daily by comparing total checks on hand to cash register totals, pre-numbered receipt totals, and mail log totals as applicable.

- Checks returned for insufficient funds should not be redeposited by the Collection Custodian. TTUHSC has established an agreement with our primary bank to automatically attempt to redeposit all insufficient funds checks. TTUHSC is not notified of an insufficient funds check until after the bank has attempted redeposit per this agreement, and the related funds are deducted from TTUHSC bank accounts.

- Credit and Debit Card Collections

- Credit and debit card collections should be processed on a credit card terminal.

- Credit and debit card collections should be processed for the exact amount of the transaction. No cash advances or withdrawals should be allowed.

- Credit card terminals should be batched and settled daily with no exceptions. If multiple cashiers access a single credit card terminal, the Collection Custodian should have a log available to track the transactions for each cashier. This allows for a single, daily batch submission for each terminal.

- A batch settlement report and terminal summary report should be printed as documentation for receipt of payment.

- Verification and Delivery of Funds Collected to Deposit Custodian

- Funds to be deposited (including cash and other forms of payment) should be summarized daily on a deposit worksheet or daily activity report that includes a summarization of each type of collection to be deposited (e.g., cash, check, credit card).

- Amounts summarized by collection type (e.g., cash, check, credit card) should be balanced to supporting documentation evidencing receipt of payment, including cash register reports, pre- numbered receipt totals, mail log totals, batch settlement reports, terminal summary reports, or other reports from computerized collections systems. Any reconciling differences should be documented.

- Cash and other forms of payment should be stored in a locked safe or similarly secured area until delivered to the Deposit Custodian for actual deposit into TTUHSC Depository Bank Accounts.

- Funds to be deposited (including cash and other forms of payment) and associated supporting documentation should be hand-delivered promptly to the Deposit Custodian for deposit into TTUHSC Depository Bank Accounts. TTUHSC requires the timely deposit of funds. Funds received must be deposited within three (3) business days. Receipts totaling $500 or more must be deposited by the following business day. Certain departments or locations that do not collect revenue each day and/or determine that it is not cost-efficient to make daily deposits of cash and coin due to costs associated with armored car services may request an exception based on dollar amounts or locations. Exceptions may be established on an annual basis and must be submitted to the Executive Vice President for Finance and Operations by the close of business July 31st for consideration the following fiscal year. Exceptions must be submitted using the Exception Request Form.

- Collection Procedures

- Written Collection Procedures should be maintained by each Collection Custodian. Procedures should be revised as needed to accommodate operational changes and should be available for review at the request of Vice Presidents, Deans, Fund Managers, Accounting Services, Audit Services, or other administrative offices on an as-needed basis.

- See Written Collection and Deposit Processing Guidelines (below) for additional guidance regarding written Collection Procedures.

Guidelines for Deposit Custodian:

- Verification and Receipt of Funds Collected from Collections Custodian

- Funds to be deposited (including cash and other forms of payment) should be verified to supporting documentation evidencing receipt of payment, including cash register totals, pre-numbered receipt totals, mail log totals, batch settlement reports, and terminal summary reports.

- All shortages greater than $10 must be reported immediately to Accounting Services. Accounting Services will determine the action necessary to reimburse the account and/or to record the shortage in the financial system.

- All shortages greater than $100 or losses, regardless of amount, occurring from known or suspected theft must be reported immediately upon discovery to Audit Services, the Texas Tech Police Department, and Accounting Services.

- Daily Reconciliation to Bank Activity Report

- Each Deposit Custodian must have a daily procedure in place to reconcile or match deposits received from collection custodians to deposits shown on the previous day's bank activity report. Outstanding or unreconciled transactions must be investigated and resolved immediately.

- A list of completed cash receipts and the supporting bank activity report should be forwarded to the Student Business Services Office in Lubbock on a daily basis. This documentation should be emailed to the Student Business Services Office at SBSCashReceipts@ttuhsc.edu. If a deposit location does not have any receipts on a particular day, the Student Business Services Office should be notified via email.

- A copy of the previous day's bank activity report should be submitted to the Student Business Services Office as supporting documentation for related cash receipts.

- Daily reconciliation supporting documentation, including a list of completed cash receipts and the previous day's bank activity report, should be retained for no less than four years.

- Deposits of Funds Collected

- TTUHSC requires the timely deposit of funds into TTUHSC Depository Bank Accounts. Funds received must be deposited within three (3) business days with no exceptions. Receipts totaling $500 or more must be deposited by the following business day. Certain departments or locations that do not collect revenue each day and/or determine that it is not cost-efficient to make daily deposits of cash and coin due to costs associated with armored car services may request an exception based on dollar amounts or locations. Exceptions may be established on an annual basis and must be submitted to the Executive Vice President for Finance and Operations by the close of business July 31 for consideration the following fiscal year. Exceptions must be submitted using the Exception to Timely Deposit of Funds form. When it is necessary to store funds overnight, adequate safeguarding must be provided by the applicable custodian.

- Check dates should be monitored to ensure compliance with State law regarding prompt deposits. Collection Custodians should be notified in writing of failure to comply with State law. In the event of a second occurrence, the next higher level of administration for the Collection Point and Audit Services should be notified of noncompliance.

- All funds deposited to a TTUHSC Depository Bank Account should be documented using duplicate deposit slips. Copies of bank-validated deposit slips should be kept on file by the Deposit Custodian for the current fiscal year and three previous fiscal years.

- Cash Receipt Preparation

- Revenue deposits are recorded in TTUHSC’s Banner Finance System utilizing the Cash Receipts system per HSC OP 50.26 Use of Online Cash Receipts System. Gifts for the benefit of TTUHSC that are processed by Texas Tech Foundation Inc. do not utilize the Cash Receipts system.

- Training regarding the use of the Cash Receipts system is available under the Help menu within that system in the Cash Receipts Help document.

- Batch settlement reports and terminal summary reports should be uploaded into the Cash Receipts system for all cash receipts recording credit card collections. If either the batch settlement report or the terminal summary report is not printed on standard-size paper, it must be taped to a standard sheet of paper to be attached to the cash receipt.

- Cash receipts should be entered in an expeditious manner. Interest is allocated to TTUHSC funds based on the day that the cash receipt is posted in the Banner Finance System. Thus, a delay in entering a cash receipt will negatively impact the allocation of interest earnings to TTUHSC funds.

- If the FOP information necessary to properly complete the cash receipt is unknown, the cash receipt should be completed in accordance with HSC OP 50.35 Unidentified Receipts and Holding Account Maintenance.

- Overage amounts for revenue collected and deposited into educational and general funds should be recorded on a cash receipt to FOP 101041-201312-NG, using account 570000. Overage amounts for revenue collected and deposited on other non-E&G funds should be recorded on a cash receipt to the applicable FOP using account 570000.

- Cash receipts recorded to an expense account should contain the original Banner finance document ID in the description block of the cash receipt. If the deposit is based on a purchasing card transaction, the description should identify the bank statement date and applicable document ID. All deposits for reimbursements or refunds to procurement card transactions must be sent to the Purchasing Card Coordinator in Payment Services.

- Collection Procedures

- Written Deposit Processing Procedures should be maintained by each Deposit Custodian. Procedures should be revised as needed to accommodate operational changes and should be available for review at the request of Vice Presidents, Deans, Fund Managers, Accounting Services, Audit Services, or other administrative offices on an as-needed basis.

WRITTEN COLLECTION AND DEPOSIT PROCESSING PROCEDURES

General Requirements:

Each Collection Custodian and Deposit Custodian should maintain written procedures to document compliance with this Deposit Procedures manual and related TTUHSC Operating Policies. Written procedures should be evaluated and revised routinely to accommodate operational changes. Written procedures should be available for review at the request of Vice Presidents, Deans, Fund Managers, Accounting Services, Audit Services, or other administrative offices on an as-needed basis.

Each Vice President or Dean with responsibility over operations that include Collection Points and Deposit Processing Points bears the responsibility for the respective procedures in his/her area. These individuals should review written procedures to ensure compliance with this manual and related TTUHSC Operating Policies. Additionally, these individuals should ensure that respective departments are following the established procedures.

Fund managers are ultimately responsible for verifying that collections and deposits posted to their respective funds are accurate and complete. Thus, fund managers should review written procedures to obtain a comfort level that their collections and deposits are handled appropriately according to requirements contained in this manual and related TTUHSC Operating Policies.

Informational Requirements:

Basic informational requirements for written Collections and Deposit Processing Procedures are outlined below. Written procedures will vary based on the organization of each TTUHSC department containing Collection Points and/or Deposit Processing Points. Further written Collections Procedures and Deposit Processing Procedures may be developed as separate documents or combined into a single document, depending on the organization of each TTUHSC department containing Collection Points and/or Deposit Processing Points.

- Basic Information

- Name and title of Collection Custodian and/or Deposit Custodian

- Name and title of Cash Handlers

- Location of each Collection Point and/or Deposit Processing Point

- Sources of collections processed by each Collection Point.

- Location of Collection Points processed by each Deposit Processing Point

- Location of Deposit Processing Point

- Supporting Documentation for Collections

- Description of types of collections received by the Collection Point (cash, check, credit card, etc.)

- Supporting documentation requirements for each type of collection (register receipts, pre- numbered receipts, mail log, batch settlement report, terminal summary report and/or other reports from computerized collections systems) including any variations when received in person or received by mail.

- Daily Operations, Reconciliation and Balancing

- Daily balancing and reconciliation procedures to be used at each Collection Point and Deposit Processing Point must be documented in detail.

- Process for refusal of postdated, third-party, or altered checks.

- Process for ensuring that checks are properly endorsed in accordance with HSC OP 50.10 Endorsement Stamps and Endorsement of Checks.

- Description of routine daily operations such as entering deposits in the Cash Receipts system including a description of review and approval requirements.

- Process for daily delivery of collections from the Collection Point to the Deposit Processing Point.

- Procedure for resolving discrepancies between amounts reported by the Collection Custodian and amounts received by the Deposit Custodian should differences occur.

- Segregation of Duties and Internal Controls

- Process for ensuring that the functions of Collections and Deposit Processing are exclusively separated and not overseen by one individual.

- Requirements regarding cashier access to cash drawers at Collection Points.

- Requirements for routine balancing of cash drawers at Collection Points and oversight of related cash funds per requirements TTUHSC OP 50.21 Cash Funds.

- Process for reviewing and approving voided receipts or other transactions.

- Identification of person or persons responsible for reviewing and approving exceptions, such as cash drawers being out-of-balance, voided transactions approved by Collection Custodians, overages/shortages reported and entered by Deposit Custodians, etc.

- Safeguarding of Funds

- Description of the secure storage of cash and other forms of payments and other related materials (e.g., endorsement stamps, deposit slips, etc.) before, during, and after business hours.

- Process for ensuring that only personnel with appropriately designated job functions are permitted access to cash and other forms of payments and other related materials.

- Training of Personnel

- Process for ensuring that all personnel involved in the Collection and Deposit Processing functions are adequately trained.

Requirement to complete and retain documentation regarding completion for any required training, such as Cash Fund Training per TTUHSC OP 50.21 Cash Funds.

Contact

Finance Systems Management

-

Address:

3601 4th Street STOP 6209 | Lubbock, Texas 79430-6209 -

Email:

fsm@ttuhsc.edu