Program Codes

Program Codes

Program codes classify the function of expenses to reflect the mission-related purpose of the expenses as established by the National Association of College and University Business Officers (NACUBO). Program codes are used to categorize expenses and denote why expenses were incurred for the Annual Financial Report (AFR), the Facilities and Administration Rate Study (formerly Indirect Cost), and other various reporting requirements.

Program Codes are assigned to Fund Codes when new funds are established through the Fund Maintenance System, New Fund Request module. Program Codes are defaulted to all Fund Codes to allow departments to easily classify expenses into mission-related purposes with minimal interaction.

Department's Responsibility

Departments must ensure the proper default Program Code is accurately assigned to all new and existing Fund Codes and understand how to properly classify expenses to help ensure accurate expense financial reporting.

Fund Codes generally utilize only the default Program Code for expense classification. Departments should ensure all revenue, expenses, and transfers are coded to the default Program Code. One exception to this rule pertains to funds that have the following default Program Codes:

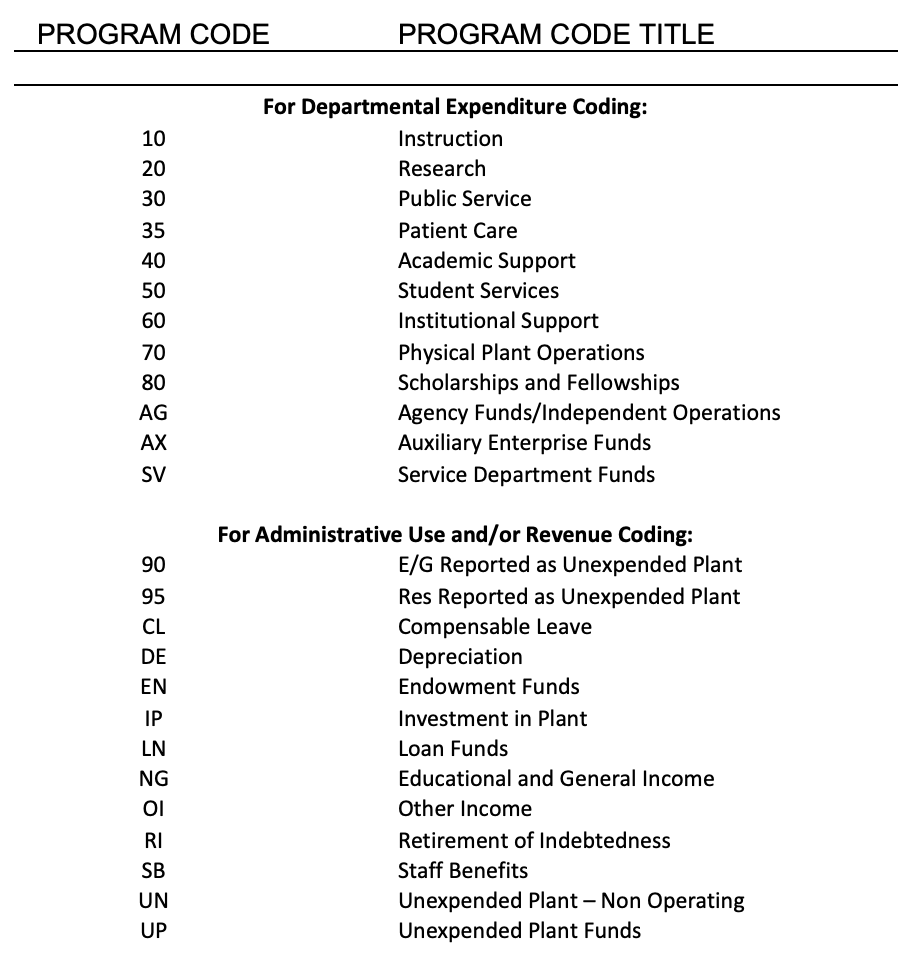

10 - Instruction

35 - Patient Care

40 - Academic Support

These three Program Codes can be used within one fund since these functions are so closely related. The department is responsible for ensuring that a budget is established for each program code used within a fund, and expenses are accurately classified in the correct Program Code.

To determine a fund's Program Code default, go to Cognos, follow the path: Team Content > HSC Finance > Chart of Accounts and select the Default Org and Program Codes report.

Program Codes

Program Definitions

10 - Instruction - Includes expenditures for all activities that are part of an institution's instruction program. Expenditures for credit and noncredit courses; academic, vocational, and technical instruction; remedial and tutorial instruction; and regular, special, and extension sessions should be included.

20 - Research - Includes all expenditures for activities specifically organized to produce research, whether commissioned by an agency external to the institution or separately budgeted by an organizational unit within the institution. Subject to these conditions, the category includes expenditures for individual and/or project research as well as that of institutes and research centers.

30 - Public Service - Includes expenditures for activities established primarily to provide non-instructional services beneficial to individuals and groups external to the institution. Included in this category are conferences, institutes, general advisory services, reference bureaus, radio and television, consulting, and similar non-instructional services to particular sectors of the community.

35 - Patient Care - Includes expenditures for activities for patient care but not related to instruction. This category includes clinic nurses and clinic support staff.

40 - Academic Support - Includes expenditures to provide support services for the institution's primary missions: instruction, research, and public service. Included in this category are the retention, preservation, and display of educational materials; the provision of services that directly assist the academic functions of the institution; media such as audio-visual services and technology such as computing support; academic administration (including academic deans but not department chairpersons) and personnel development providing administration support and management direction to the three primary missions; and separately budgeted support for course and curriculum development.

50 - Student Services - Includes expenditures for offices of admissions and the registrar and activities with the primary purpose of contributing to students' emotional and physical well-being and intellectual, cultural, and social development outside the context of the formal instruction program. Included in this category are expenditures for student activities, cultural events, student newspapers, intramural athletics, student organizations, counseling and career guidance, student aid administration, and student health services.

60 - Institutional Support - Includes expenditures for central executive-level activities concerned with management and long-range planning for the entire institution, such as the governing board, planning and programming, and legal services; fiscal operations, including the investment office; administrative information technology; space management; employee personnel and records; logistical activities that provide procurement, storerooms, safety, security, printing, and transportation services to the institution; support services to faculty and staff that are not operated as auxiliary enterprises; and activities concerned with community and alumni relation, including development and fundraising.

70 - Physical Plant Operations - Includes all expenditures of current operating funds for the operation and maintenance of the physical plant. Included in this category are all expenditures for operations established to provide services and maintenance related to grounds and facilities. Also included are utilities, fire protection, property insurance, and similar items.

80 - Scholarships and Fellowships - Includes expenditures for scholarships and fellowships from current funds in the form of grants to students, resulting from selection by the institution or from an entitlement program. The category also includes trainee stipends, prizes, and awards. Trainee stipends awarded to individuals who are not enrolled in formal coursework should be charged to instruction, research, or public service.

AG - Agency Funds/Independent Operations - Includes expenditures related to Agency funds. Agency funds belong to the agency (not TTUHSC) which earns the associated revenue, and are used to support the activity of that agency. As a courtesy, TTUHSC allows the related agency to use our finance system to account for its activities. Agency funds include funds that are set up for TTUHSC student organizations and for other TTUHSC groups or activities.

AX - Auxiliary Enterprises - Includes expenditures related to Auxiliary Enterprises funds. An auxiliary enterprise exists to furnish goods or services to students, faculty, or staff, and charges a fee directly related to, although not necessarily equal to, the cost of the goods or services. The distinguishing characteristic of an auxiliary enterprise is that it is managed as an essentially self-supporting activity. Examples are residence halls, food services, college stores, faculty clubs, faculty and staff parking, and faculty housing.

SV - Agency Funds/Independent Operations - Includes expenditures related to an established Service Department. A Service Department provides goods and services to other departments within the institution. May only be used on Service Department funds (type 19).

If you have additonal questions, contact Accounting Services at hscacc@ttuhsc.edu.

Contact

Finance Systems Management

-

Address:

3601 4th Street STOP 6209 | Lubbock, Texas 79430-6209 -

Email:

fsm@ttuhsc.edu